What will the Construction and Infrastructure Market look like Post-COVID and How Do We Best React to it?

With the outbreak of COVID-19, the forecast for Construction and Infrastructure looked bleak. In March 2020 these markets were confronted with a miserable cocktail of site work stoppages, supply chain interruptions, and contract suspensions. The resultant liquidity challenges and funding gaps felt doubly frustrating given that the government had only months before announced their commitment to investing in construction through the £100bn National Infrastructure Strategy.

Undoubtedly, COVID-19’s primary impact on Construction and Infrastructure has been that of widespread and forced change. However, for all the havoc wreaked by the virus, there are three myths that need dispelling. Firstly, that the pandemic has only served to affect these industries for the worse. There have in fact been great opportunities created by the pandemic. In many cases, contingency measures initially adopted in haste have since been developed and implemented as best practice. This symbolises a new way of working in Construction and Infrastructure, characterised by flexibility, agility and efficiency.

Secondly, the pandemic does not represent a seismic shift or turning point for the Construction and Infrastructure sectors. Many features of today’s markets can be traced back to initiatives with pre-pandemic roots – COVID-19 was simply the catalyst that forced the hand of modernisation.

Thirdly, the notion of a ‘post-COVID’ market is in itself something of a fallacy. A far cry from the Prime Minister’s statement in March 2020 that we could ‘turn the tide’ of the virus in just 12 weeks, most of us have now accepted that COVID-19 is not going to disappear anytime soon and that we must evolve to work around it. Which, as per point one, is not necessarily a bad thing.

What Will the Market Look Like?

When we envisage a post-COVID market, we might imagine a landscape bereft of construction and innovation. Yet this has not proven to be the case. A survey conducted by New London Architecture shows that the pandemic has not resulted in any sustained downturn of construction work in the capital. The current pipeline of work has risen by almost 8% since 2019, with the number of buildings in either planning or construction rising from 544 to 587 [1].

Buildings either under planning or construction in London, 2019 to 2021

In infrastructure too, there will be no shortage of work as the government continues to prioritise and pursue ambitious fibre rollout targets. Far from undermining it, the pandemic has emphasised the need for significant investment in telecommunications infrastructure, since a reliable internet connection is a crucial ingredient of successful remote working.

Rather than sabotaging the growth of the Construction and Infrastructure sector, the pandemic has merely reshaped priorities. As ‘work from home’ practices look set to be perpetuated beyond the pandemic, it is unlikely that we will see a return to the pre-COVID office working model. As a result, contractors and investors should take note of the wider geographical scope of the post-COVID market. In London, the capital’s outer boroughs now account for almost 40% of new ‘tall buildings’ (20 storeys or higher) [1], suggesting that efforts to keep pace with housing targets are increasingly concentrated in the suburbs rather than in more central postcodes.

Indeed, the post-COVID market looks set to become less London-centric altogether. 700,000 people moved out of the capital in 2020 alone [2], and as companies become increasingly devolved there is no reason to think the demand for regional infrastructure will subside. More than ever, contractors are looking beyond the London skyline for the best opportunities. A London-based developer has recently been granted a £175m contract for the redevelopment of Bristol’s Soapworks public space, with Project Director Lucinda Mitchell stating that the construction of 140,000 sq. ft. of flexible workspace will “help drive Bristol’s economic recovery from COVID-19” as “corporates shift to a decentralised ‘hub and spoke’ office model” [3].

Bristol Soapworks Development

This trend is also being mimicked elsewhere across the infrastructure sector. In telecoms, Openreach has committed to rolling out fibre to 3.2 million properties in rural areas, with the government pledging to pick up any slack [4]. The post-COVID market is one where centrality is no longer synonymous with desirability.

However, although COVID-19 has refocused the target of investment in Construction and Infrastructure, it has not fundamentally changed the long-term aims of these sectors. In fact, more often than not, COVID-19 has accelerated the development of goals such as sustainability, innovation and flexibility which stakeholders previously recognised as important but did not have the impetus to enact. In this light, we can view COVID-19 as a helpful catalyst that has enabled these industries to rethink their ways of working.

How Can We Best React?

For this reason, we can best react to COVID-19 by treating it as a learning process and allowing it to inform our decision-making. The pandemic has exposed the need for proactive strategies and the implementation of robust, future-proof processes. In light of minimised face-to-face contact, it has also shown the importance of aligning cultures and behaviours across supply chains.

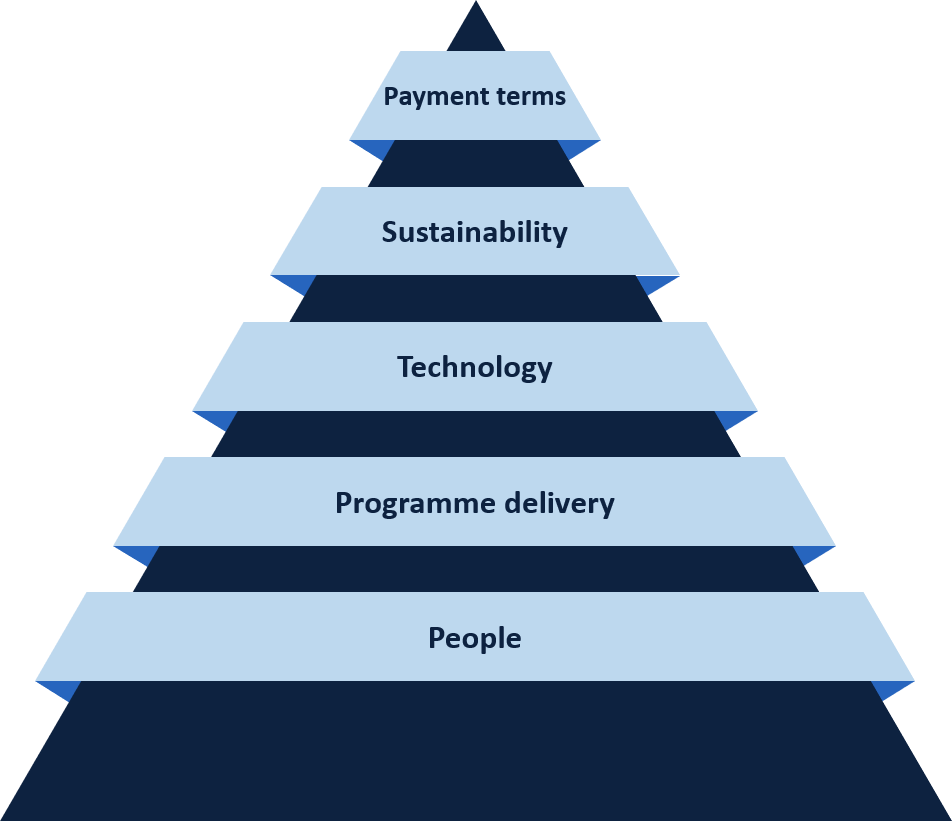

At Deecon we have identified five key areas where Construction and Infrastructure stakeholders can harness the changes brought about by the pandemic to realise longer-term goals. These are:

Payment terms: The pandemic highlighted the crucial importance of cash flow within Construction and Infrastructure contracts. We help our clients to devise robust payment terms and to foster trust with their suppliers to protect cash flow.

Sustainability: The increased emphasis on sustainability and ‘building back better’ caused by COVID-19 has created renewed enthusiasm for quality. By focusing on the procurement of high-quality goods and longer-term partnerships, our clients are better protected against future contract disruptions.

Technology: Communication, works management and CVR systems had to be quickly deployed to adapt to new working patterns and logistical challenges caused by COVID-19. We work with our clients to implement these processes not as a stop-gap, but as a long-term solution that reduces reliance on manual intervention.

Programme delivery: COVID-19 can be an opportunity for a fresh start on delayed and poorly performing contracts. Through the implementation of improved delivery strategies and communication channels, clients can derive increased benefit out of their contracts.

People: We are supporting clients to manage the ‘new normal’ with a focus on enhanced H&S and wellbeing, in addition to strategic mitigation against the projected labour shortages and skills gaps.

Five pillars of resilience in a post-COVID world

These five pillars show that lessons learned during COVID-19 are pushing the sector to modernise and improve. Consequently, the post-COVID market will be characterised not just by recovery but by aspiration, and stakeholders can best react by embracing this approach.

Lastly, we can react effectively to COVID-19 by not letting it eclipse other emerging challenges in the market. Pandemic-hysteria has surely masked the effects of Brexit on the Construction and Infrastructure sectors, so we should be mindful of how labour resources and supply chains are being impacted by the new climate and mitigate accordingly.

It is important to remember that these markets are dynamic landscapes undergoing constant evolution, with the pandemic representing only the most recent disruption of many. We started this article with 3 myths, so it seems apt to conclude it with 3 truths. One – the Construction and Infrastructure industries have seen challenges before. Two – there will certainly be more challenges to come. But thirdly and most importantly – the resilience of these markets should not be underestimated.